Opportunities for investment return treats exist in many sectors and securities as we enter the backdrop of a historically favorable November-April money flow season and mid-term election cycle. Still, tricky twists, feelings of lost control, and shadows of uncertainty may loom just around the corner. Central Banks bear the queasy burdens where politicians and ugly structural dynamics fail to deliver the goody bags. Broader markets could be in for a real scare or two so our smart preparation will translate into a steadier pulse if fear really accelerates. Lessen the potential for emotional decision-making and focus on those things which can be better controlled. Please review the concluding checklist to help control your fears and advantageously position your comprehensive plan.

Opportunities for investment return treats exist in many sectors and securities as we enter the backdrop of a historically favorable November-April money flow season and mid-term election cycle. Still, tricky twists, feelings of lost control, and shadows of uncertainty may loom just around the corner. Central Banks bear the queasy burdens where politicians and ugly structural dynamics fail to deliver the goody bags. Broader markets could be in for a real scare or two so our smart preparation will translate into a steadier pulse if fear really accelerates. Lessen the potential for emotional decision-making and focus on those things which can be better controlled. Please review the concluding checklist to help control your fears and advantageously position your comprehensive plan.

Not Quite Campfire Worthy–A Tale to Set the Scene

One beautiful fall day in 2014, they walked along the streets paved with greenbacks. The skies were blue, and the air was refreshingly crisp. Perhaps ready to embark on a different journey, they reminisced the ups and downs of a six year history since the miserable fall of 2008. Tears and smiles were shared as they chronicled times of fear and euphoria. At some point on this fine day, the road became twisted, winding aimlessly, briefly directionless. The skies were suddenly grayer and less reflective. Look! Ahead there…a house! An eagle sculpture above the federal entrance signaled prestige and power. They huddled, and the group thought, this place will provide the guidance we seek. They approached the monumental iron doors and grasped the ice cold lion’s head door knocker. A pleasant and welcoming white haired hostess invited them in as the door slowly creaked open. The foyer was extremely bright with sudden flashes of extreme darkness. The new air felt cold as it occassionally drifted across the back of their necks. The smell turned foul as the uninvited musty taste breached their tongues. BOOM! The door abruptly shut behind them, and despite the hostess’s assurances of safety, the group’s confidence and expectations were terribly shaken…

The World Relies on the U.S. Federal Reserve

October 29th marks the next scheduled policy announcement from the most powerful central bank in the world, and investors, media, and politicians will parse every word for signs of confidence and expert guidance. U.S. monetary policy is made by the Federal Open Market Committee (FOMC), which consists of the members of the Board of Governors of the Federal Reserve System and five Reserve Bank presidents. The FOMC holds eight regularly scheduled meetings during the year, and it is widely anticipated that the Committee will officially cease material additions to its QE3 bond buying program at October’s meeting.

A few key goals of this so-called Quantitative Easing (QE3) program:

- maintain downward pressure on longer-term interest rates

- support mortgage markets

- help to make broader financial conditions more accommodative, which, in turn, should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate

All three QE3 goals impact your retirement portfolios, college savings accounts, and “fun money” brokerage accounts. Your willingness to become an astute watcher of market inputs such as FOMC activity and the inverse relationship between interest rates and bond prices will increase your basic understanding of fluctuating account values, and it will enhance your potential success as an individual investor and consumer of financial advice. Never rely 100% on an advisor with sole discretion over your accounts and the directive, “just make me money!”

Thank you to my friends at Intrinsic Research for supplying charts for three of the key market proxies spooked this October: daily S&P 500 stock index, weekly US 10-Year Bond yields, and weekly Crude Oil prices. Explanations for soaring market volatility range from Ebola, terrorism, European woes, politics, and concerns over top-line revenue growth. Bottom Line: The complacency of clearer skies has been replaced with a cloudier picture; whereby professional, novice, and machine-driven traders demonstrated an ability to accelerate out of assets such as lower rated corporate bonds and stocks.

Current Chair of the Federal Reserve, Dr. Janet Yellen, has pointedly reiterated that interest rate targets are “data-dependent” and not based on a calendar projection; that is, when economic conditions and the economic outlook warrant a less accommodative monetary policy, the Committee will raise its range for the benchmark interest rate it targets (federal funds rate). Many powerful market participants are betting that early to mid-2015 will mark the beginning of a new higher rate regime. This dynamic relationship between two sometimes opposing forces (central banks & traders) will likely cause great angst, volatility, and uncertainty in many portfolios over the coming quarters as the Federal Reserve attempts to tip-toe in and out of the lurking economic shadows. Home mortgages, business loans, corporate deal-making, global trade, a range of asset classes, currencies, and critical decisions will be impacted. Make sure to solidify your well grounded short and long-term plans in order to avoid the emotional decision-making that overwhelms so many people at dark moments.

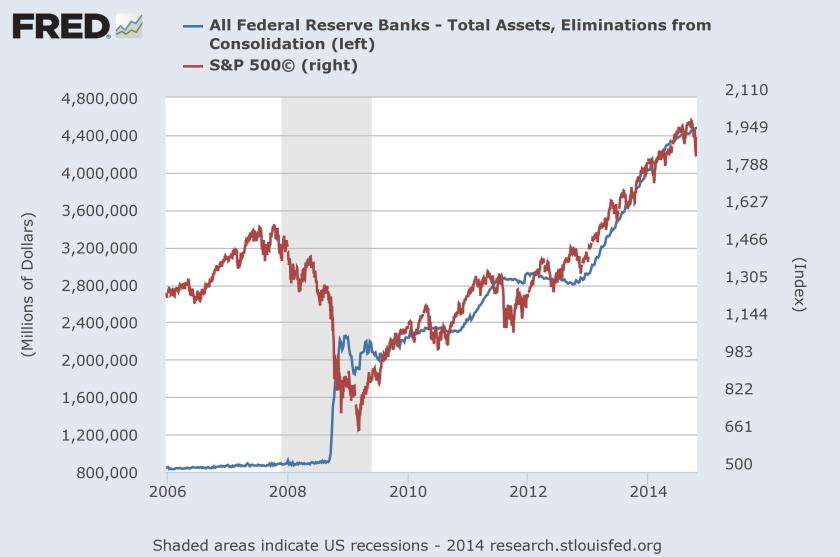

A Famous Chart & Unprecedented Efforts

As provided by the St. Louis Fed’s fantastic FRED database and courtesy of S&P Opco, LLC, the below graph illustrates the total assets of the Federal Reserve, which have grown considerably from $869 billion pre-crisis levels during the summer of 2007 to today’s levels of nearly $4.5 trillion (left-axis). The leader of this growth effort is an American Hero, Dr. Ben Bernanke, former Fed Chair, who succeeded Alan Greenspan in February 2006. Bernanke’s outstanding reputation included his thorough studies on The Great Depression and Japanese deflation. In 2002, one of Bernanke’s first speeches as a Federal Reserve Governor, was entitled “Deflation: Making Sure ‘It’ Doesn’t Happen Here.” A so-called Bernanke Doctrine emerged to identify specific measures required to combat or prevent deflation. There is little doubt that heroic actions were taken during the Great Financial Crisis of 2007-2009, and there is little doubt that the S&P 500 stock index (right-axis) benefitted greatly from unprecedented and continuous support.

Deflation is in almost all cases a side effect of a collapse of aggregate demand – a drop in spending so severe that producers must cut prices on an ongoing basis in order to find buyers. -Dr. Bernanke

Bernanke theorized that a central bank should always be able to generate inflation. Ironically, I believe the Federal Reserve’s decision to continually add post-crisis stimulus through QE2 and QE3 programs, its attempts to modify the natural course of business cycles, and its promotion of a whatever it takes now and forever rhetoric has actually aided and abetted other deflationary forces. Of course, a strong argument can be made that other parts of Washington failed to be as heroic in efforts to restore our sub-optimal economic growth and prosperity.

Global debt burdens, demographics, impacts of technology, skills degradation, and plummeting velocity of money are structural forces that compete hard against Dr. Bernanke and his best laid plans. -Michael (no doctorate)

Global stocks, bonds, property, and numerous other assets’ prices have risen and probably contributed to some rough wealth effects; that is, some aggregate upward change in demand encouraged by more spending and less saving. Of course, a major risk factor is the potential reflation of yet another set of asset bubbles caused by excess central bank liquidity and credit rather than “fixing” economic fundamentals. Whatever the case, it is hard to argue “mission accomplished” as large and small economies face growth fears and fragility this fall of 2014. Therefore, any change in U.S. monetary policy runs the risk of igniting a chain reaction of extreme volatility throughout the globe.

Smart Preparation Goes A Long Way

As the Federal Reserve soon attempts to lead a new confident path, a trajectory of structural resolutions is unclear and negative side effects loom large. I fear Bernanke’s, and now Yellen’s, traditional econometric modeling will reveal numerous break downs in theory as the Federal Reserve shifts its unconventional policies. Unfortunately, market players put too much faith in the ability of humans (or machines for that matter) to legitimately map flawless outcomes for real growth, unemployment levels, interest rates, credit markets, and behavioral reactions. Smart market strategists believe the European Central Bank (ECB) will take the global baton with its own rumored unconventional programs. Again, not a fix for long-term structural problems, and this notion of a global market fully confident and supported by a non-unified group of Euro Nations to replace the United States Federal Reserve provides no comfort to this investor.

Previous attempts by the FOMC to exit QE programs in March 2010 and June 2011 were met with significant volatility and lower asset prices.

The FOMC’s announcement on October 29th may not spook market participants due to its widely anticipated outcome; however, just like expecting to be scared at a Halloween haunted house, an expected “BOO!” can still raise the hair on your arms and make you jump! Let’s avoid complacency or delays in necessary portfolio adjustments even if financial markets seem settled and the S&P 500 (1,971) again surpasses the 2,000 level. The next Summary of Economic Projections and press conference by Chair Yellen (pictured) will be December 17, 2014: It is sure to be interesting and educational!

The FOMC’s announcement on October 29th may not spook market participants due to its widely anticipated outcome; however, just like expecting to be scared at a Halloween haunted house, an expected “BOO!” can still raise the hair on your arms and make you jump! Let’s avoid complacency or delays in necessary portfolio adjustments even if financial markets seem settled and the S&P 500 (1,971) again surpasses the 2,000 level. The next Summary of Economic Projections and press conference by Chair Yellen (pictured) will be December 17, 2014: It is sure to be interesting and educational!

Focus on more controllable fear factors:

The below topics are important, and I wish to

empower you with more specific tools, tips, and experience.

I feel strongly about efforts to shape a trustworthy, forward-thinking

financial industry where families’ interests are served first.

- Communicate, Educate, Empower with all close family members;

- Take charge of the collaboration amongst your tax, legal, and business advisors to maximize your family’s financial, tax, and investment planning–do not assume this is taking place without your encouragement;

- Assess your family’s unique growth, income, tax, risk tolerances, and asset location needs–be your best advocate and communicate with your advisors;

- Revisit portfolio diversification within and across all taxable & tax-deferred accounts–examine holdings beyond broad buckets of stocks, bonds, cash to ensure comprehensive suitability, proper risk alignment, and balance;

- Be more selective with the evaluation of reward-to-risk factors among your individual securities and less reliant on “a rising tide lifts all boats” strategy;

- Note: Cash is an important asset class with its own characteristics of safety

and future opportunity–even worth paying a fee upon;

- Maximize retirement strategies (Social Security, Roth, 401k, insurance);

- Know all your costs such as quarterly fees based on assets, transaction costs on trades, additional fees not easily seen from owning and trading mutual funds, closed-end funds, and exchange-traded-products–hint, the trend is down; and

- Check conflicts of interest (too many to list) among your advisors, investments owned, products sold, trade execution & allocation, and actual services rendered versus those promised before you signed the dotted-line

Previously, I suggested that the FOMC invest in a classic econometric tool (a family game of Monopoly) to simulate what happens when you dramatically change the rules of the game and then attempt to “normalize” back–not pretty: http://bit.ly/1uFITDA

+++

I welcome your comments.

Michael embodies client-stewardship in all his work and happens to be a passionate expert in securities analysis, asset allocation, economic analysis, and wealth management solutions.

Email: mdhakerem@gmail.com & Twitter: @MichaelHakerem

Photo Courtesy of U.S. Federal Reserve: Eccles Building 1937

Photo Courtesy of IMF Staff Photograph/Stephen Jaffe: Dr. Janet Yellen

The S&P 500 index is proprietary to and is calculated, distributed and marketed by S&P Opco, LLC (a subsidiary of S&P Dow Jones Indices LLC), its affiliates and/or its licensors and has been licensed for use. S&P® and S&P 500®, among other famous marks, are registered trademarks of Standard & Poor’s Financial Services LLC, and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. © 2014 S&P Dow Jones Indices LLC, its affiliates and/or its licensors. All rights reserved.

opy.) of the real orchestrated manipulation that impacts us today dates back many Lunar

opy.) of the real orchestrated manipulation that impacts us today dates back many Lunar

he fast-paced world of real estate and finance. Each smiled and contemplated the wheeling and dealing for property, houses, hotels and GET OUT OF JAIL FREE cards.

he fast-paced world of real estate and finance. Each smiled and contemplated the wheeling and dealing for property, houses, hotels and GET OUT OF JAIL FREE cards.